summary:

The Federal Reserve just cut its benchmark interest rate again, and the immediate, Pavlovi...

summary:

The Federal Reserve just cut its benchmark interest rate again, and the immediate, Pavlovi... The Federal Reserve just cut its benchmark interest rate again, and the immediate, Pavlovian response from the public is predictable: mortgage rates must be about to plummet. It’s a simple, appealing narrative. The Fed, in its wisdom, pulls a lever in a Washington D.C. boardroom, and somewhere across the country, a family’s dream home becomes more affordable. The problem with this narrative is that it’s mostly fiction.

The data from the past year paints a picture not of clean cause-and-effect, but of a messy, unreliable correlation. Looking at the Fed's actions versus the actual borrowing costs for homebuyers reveals a significant disconnect. The federal funds rate is a blunt instrument designed to influence short-term interbank lending. Mortgage rates, on the other hand, are a different beast entirely, driven by the far more complex and forward-looking market for long-term debt.

Thinking the Fed directly controls your 30-year fixed rate is like believing the person who sets the thermostat in an office building also controls the weather outside. One is a localized, direct input; the other is a vast, chaotic system influenced by a thousand different variables. And right now, the market is telling us the weather isn't changing just because the Fed turned down the AC. I’ve analyzed these patterns for years, and the market’s predictive pricing often creates the illusion of a direct cause-and-effect that simply isn’t there. The truth is in the numbers, and they tell a far more complicated story.

The Illusion of Control

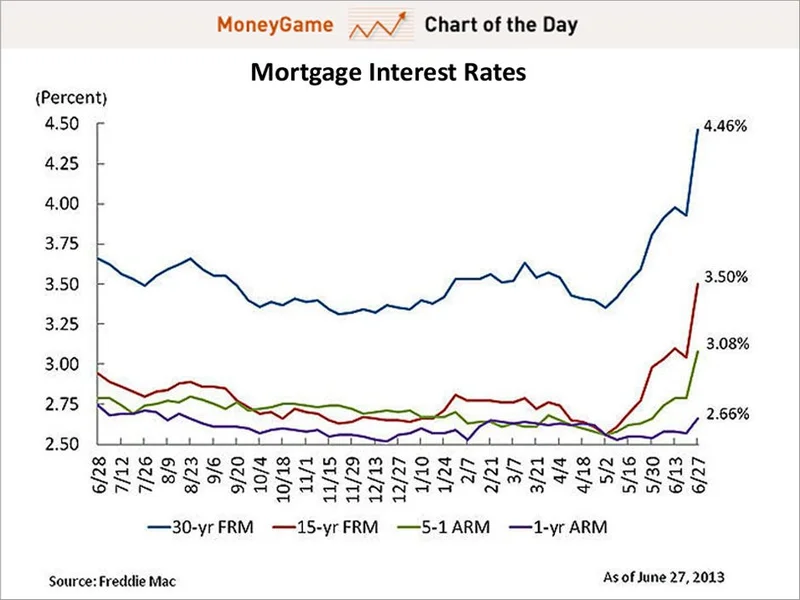

Let’s rewind to September 2024. The Fed, after a relentless series of hikes, finally pivoted, cutting its benchmark rate by a significant 50 basis points. In the run-up to this, the average 30-year fixed mortgage rate did indeed fall to around 6.08%, its lowest point in two years. For a moment, the textbook theory held. The lever was pulled, and the intended effect seemed to follow. But the relief was fleeting. Within weeks, mortgage rates began to climb again as bond markets (where mortgage rates are truly born) digested the inflation outlook and decided they weren't convinced.

The subsequent cuts in late 2024 only reinforced this disconnect. In November 2024, the Fed delivered another cut. Mortgage rates? They had actually increased since the September move, hovering stubbornly between 6.8% and 6.9%. Then came the December 2024 cut of 25 basis points (a quarter of a percentage point). Once again, mortgage rates barely budged, closing out the year near that same 6.8% level.

What was happening here? The market for mortgage-backed securities, which is deeply intertwined with the yield on 10-year Treasury notes, was running on a completely different set of assumptions than the Fed. Lenders and investors weren't pricing mortgages based on today's federal funds rate; they were pricing them based on their forecast for inflation and economic growth over the next decade. The Fed was trying to steer the massive container ship of the economy with its small rudder, but the powerful ocean currents of market sentiment were pushing the vessel in a different direction. The data is unequivocal: three consecutive Fed cuts resulted in mortgage rates that were materially higher than before the easing cycle began.

A Glimmer of Correlation

It wasn't until a year later, in September 2025, that we saw a pattern emerge that looked more like the one consumers expect. The Fed announced another 25-basis-point cut, and this time, mortgage rates responded, dipping from the mid-6.4% range down to a three-year low of about 6.13%. So, what changed? Was the link suddenly repaired?

Not exactly. The context had shifted. By September 2025, the market had more data suggesting inflation was, if not defeated, at least stabilizing. Bond investors began to price in the possibility of a longer, more sustained easing cycle from the Fed. The rate drop wasn't a direct reaction to that day's announcement; it was the culmination of months of shifting sentiment. The market finally started to believe the Fed's actions would stick, and Treasury yields eased accordingly, pulling mortgage rates down with them. The rate fell by about a third of a point—to be more precise, from around 6.45% to 6.13%.

This brings us to today's cut. Fed Cuts Interest Rate Again as Layoffs Mount: What it Means for Mortgages as Markets React - Realtor.com. We are once again at a crossroads. Will this latest 25-basis-point reduction follow the disappointing pattern of late 2024, where the market essentially shrugged it off? Or will it build on the momentum from September 2025, nudging rates further down? The honest answer is that the Fed's action itself provides very little predictive power.

The variables that truly matter remain the same: upcoming inflation reports and the corresponding movement in 10-year Treasury yields. If investors see this latest cut as a prudent step in a cooling economy, yields may fall, and mortgages could become cheaper. But if the market interprets it as the Fed getting nervous and easing too quickly while inflation ticks back up, yields could spike, and this rate cut could paradoxically be followed by higher mortgage rates. Is the Fed just confirming what the market already knows, or is it trying to lead the market in a new direction? And does the market even care to follow?

The Fed's Rate Is Not Your Rate

Let’s be perfectly clear. If you are waiting for a Fed announcement to decide when to buy a house or refinance your mortgage, you are watching the wrong signal. The historical data shows, with very few exceptions, that the federal funds rate is a poor predictor of 30-year mortgage costs. The correlation is weak, inconsistent, and often operates with a lag that makes it useless for timing the market.

The obsession with Fed meetings is a media-driven narrative that simplifies a complex reality. The real story is written in the bond market, driven by institutional investors making multi-billion-dollar bets on the future of inflation. Your mortgage rate is a tiny footnote in that much larger story.

The practical takeaway isn't to become a Treasury yield expert. It's to stop outsourcing your financial decisions to the Federal Open Market Committee. The smarter strategy has always been to focus on what you can control: your credit score, your down payment, and your income. Prepare yourself to be financially ready, so that if a favorable rate appears—driven by the true market forces—you are in a position to act. Waiting for a signal from the Fed is like waiting for a rooster's crow to make the sun rise. It might feel connected, but the data shows it’s just noise.