summary:

The numbers in a deal of this magnitude are always the first thing you see, but they’re ra...

summary:

The numbers in a deal of this magnitude are always the first thing you see, but they’re ra... The numbers in a deal of this magnitude are always the first thing you see, but they’re rarely the most important. On October 26, the news broke: Swiss drugmaker Novartis to buy Avidity Biosciences for $12 billion. The headline figure, $72 per share, represented a 46% premium over the prior closing price of `avidity biosciences stock`.

A 46% premium. Let that sink in.

In a market where valuations are scrutinized down to the decimal point, a premium of that size isn't just an offer; it's a declaration. It’s a signal that the buyer believes the target’s intrinsic value is fundamentally misunderstood by the public markets. Or, more cynically, it’s the price of desperation. My analysis suggests it’s a calculated measure of both. Novartis isn’t just buying a company; it’s buying a solution to several existential problems, and they’ve priced that solution with surgical precision.

The Anatomy of a Premium

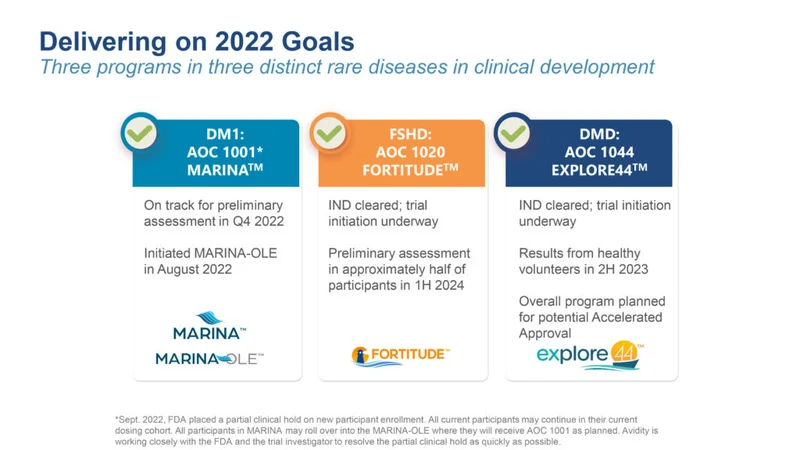

To understand the $12 billion price tag (a figure that nets out to a premium of about 46%—to be more exact, 46.5%), one has to look past the `avidity biosciences inc` letterhead and into its clinical pipeline. Avidity isn’t a speculative, early-stage biotech play. This is a company on the one-yard line. The San Diego-based firm has developed a proprietary platform for delivering RNA therapeutics, specifically antisense oligonucleotide conjugates (AOCs), directly to muscle tissue—a notoriously difficult target.

This isn't just interesting science; it’s a trio of late-stage drug candidates for devastating rare neuromuscular disorders: Duchenne muscular dystrophy (DMD), facioscapulohumeral muscular dystrophy (FSHD), and myotonic dystrophy type 1 (DM1). The company had already signaled to the market its plan to submit three approval applications over the next 12 months. The first, for its lead drug Del-zota in DMD, was expected in the first quarter of 2026.

This timeline is the entire story. Novartis isn't paying a 46% premium for a promising technology platform. It’s paying for de-risked, late-stage assets that are months, not years, away from regulatory submission. This is less like funding an expedition to find buried treasure and more like buying the treasure map when the "X" is already in sight. The premium reflects the high probability of near-term revenue streams that can help plug the enormous hole Novartis sees in its future.

The acquisition is also a validation for the entire RNA therapeutics space. While competitors like `Dyne Therapeutics` are also making strides, this deal effectively anoints Avidity’s AOC platform as a front-runner worthy of a blockbuster buyout. But what does this mean for the long-term innovation cycle? When a company that has navigated the treacherous path from its `avidity biosciences ipo` to the brink of commercialization gets acquired, does it incentivize or stifle the next generation of biotech entrepreneurs?

Novartis’s Strategic Chessboard

Looking at this from the perspective of the `novartis stock` price, the move is a masterclass in strategic necessity. CEO Vas Narasimhan’s public statements about a commitment to "devastating, progressive neuromuscular diseases" are, of course, true. But they’re also the polite corporate narrative wrapped around a much colder reality: the patent cliff.

Novartis is staring down the barrel of patent expirations for behemoth drugs like Entresto, Cosentyx, and Xolair. This isn't a distant problem; it's an impending fiscal storm. The acquisition of Avidity is like a pre-emptive infrastructure project to mitigate the coming flood. It’s not their only one, either. The purchase fits neatly into a pattern of high-stakes acquisitions, including AveXis for gene therapy (~$9B in 2018) and The Medicines Company for cholesterol drugs (~$10B in 2019). The 2024 purchase of Kate Therapeutics and other 2025 deals for Anthos and Regulus show a clear, aggressive strategy to buy, not build, its way out of trouble.

Then there’s the geopolitical layer, which is where this deal becomes particularly fascinating. I've looked at hundreds of these acquisition filings, and the timing relative to political rumblings often feels too coincidental to ignore. With a potential Trump administration threatening tariffs on Swiss goods, bulking up a U.S. presence is a shrewd defensive maneuver. Acquiring a major San Diego-based firm doesn't just add assets to the pipeline; it adds a significant operational and political anchor in the world’s largest pharmaceutical market. It’s a multi-billion-dollar hedge against a trade war.

And what of the assets Novartis didn’t want? The deal structure provides the final, crucial clue. Avidity’s early-stage precision cardiology programs are being spun off into a new entity, "Spinco." This is the tell. Novartis performed a surgical extraction, carving out the valuable, late-stage neuromuscular assets it desperately needed while leaving the riskier, early-stage programs behind for existing shareholders. It’s a clean, efficient transfer of value, ensuring Novartis pays only for the assets that solve its immediate problems. It’s the kind of ruthless efficiency you have to respect, even if it feels clinical.

A Price Tag for Certainty

Ultimately, the $12 billion figure isn't an abstract valuation of an `rna stock` company. It's a price tag for a very specific product: certainty. Novartis is paying for the certainty of three late-stage assets to refill its pipeline. It's paying for the certainty of a leadership position in the lucrative rare neuromuscular disease market. And it's paying for a hedge of certainty against geopolitical and trade-related volatility. The 46% premium isn't irrational exuberance; it's the calculated cost of solving your biggest problems in one decisive, expensive move.